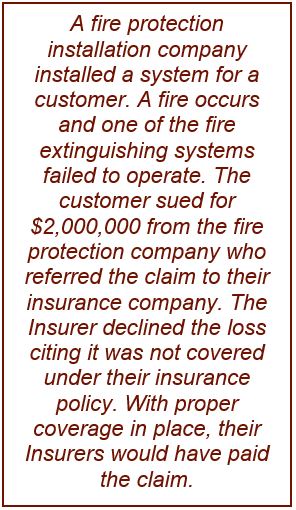

When Systems ‘Fail to Perform’ – Where’s My Insurance?

General Liability policies provide coverage when ‘something happens’ or what insurance companies refer to as an ‘occurrence’. What happens then with claims resulting from something not happening? If you are in the Electrical, Fire Protective or Security industries, everything goes wrong when your systems ‘do nothing’ instead of responding.

Isn’t this something that should be covered by my Liability policy?

Many Liability policies do not provide any coverage for these situations because they specifically exclude losses or claims arising from a ‘failure to perform’. This means that key coverage is missing, potentially resulting in expensive settlements out of pocket for any contractor involved in the manufacturing, supplying, installation or servicing of performance critical products such as fire alarms, braking systems, temperature controls, etc.

If your insurance policy does not carry “Failure to Perform” coverage, it will not pay your claim.

Who Requires This Coverage?

Sprinkler and fire protection installers & servicers

Sprinkler and fire protection installers & servicers- Electrical contractors installing a/o maintaining alarm systems

- Alarm central stations

- Security guards

- Security equipment – CCTV, intercom and access control systems

- Life and industrial safety equipment

If your company is involved in consultancy, advice, testing or design, you should also consider Professional Liability (Errors & Omissions) insurance.